Financial Reporting - CICT and Keppel Pacific Oak

CICT

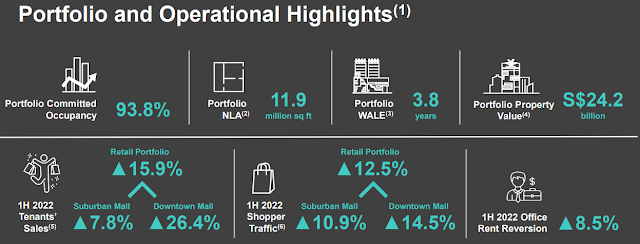

The smallest holding I have amongst the REITs. Performance within expectation.

With regards to some other metrics I look at

1. Gearing went above 40 to 40.6% from 39.1%. I normally wouldnt go for REITs with high gearing. However, I got it due to the merger of Capitaland Mall Trust and Capitaland Commercial Trust.

2. Interest Coverage went from 4.2x to 4.1x.

3. Occupancy and NAV improve slightly.

Clarke Quay will go through another AEI again. It only recently went through an AEI back in 2015. Sounds like CapitaLand is trying very hard to make it work. It's been a long time since I went to clarke quay. Is it still the place to be seen, like in 20 years ago? Guessed not.

4. DPU is consistent from the previous pay out.

1. Gearing came down from 37.5 to 37.2. Good.

2. Interest Coverage went down from 5 to 4.8. Not good but 4.8 is still a good number.

3. Occupancy and NAV improve slightly. Good.

4. DPU is slightly lower year on year due to management receiving everything in cash. Depending on how you look at it, it may be a good thing for not diluting the number of shares. However, if they are vested by getting the units, wouldn't that make them work harder to increase the share price by improving the performance?

Comments

Post a Comment